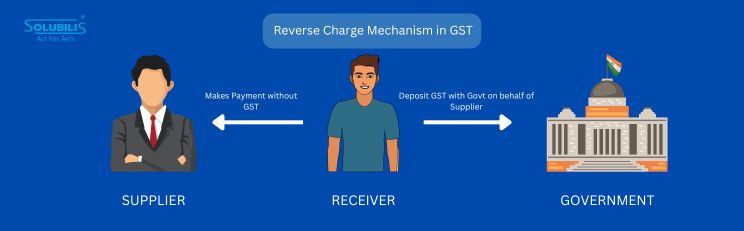

What is Reverse Charge Mechanism in GST?

In the Goods and Services Tax (GST) framework, the primary principle is that the supplier of goods or services is responsible for the payment of GST. This rule requires the collection of taxes at the point of origin, which are then remitted to the government. However, there are specific scenarios where this responsibility shifts to the recipient of goods or services under a mechanism known as the Reverse Charge Mechanism (RCM).

What is Reverse Charge Mechanism in GST?

Under the reverse charge mechanism, businesses with GST registration in Coimbatore must take on the obligation to pay GST, shifting it from the supplier to the recipient. This requires the recipient to calculate and directly pay the tax to the government, rather than the supplier.

Why Does the Reverse Charge Mechanism Exist?

The GST regime introduced the reverse charge mechanism for several reasons.

- Enhancing Tax Compliance: By shifting the tax liability to the recipient, particularly in scenarios involving unregistered suppliers or import transactions, the government ensures a higher level of compliance and accountability in the tax system.

- Expanding the Tax Net: Reverse charge widens the scope of GST by capturing transactions that might otherwise go unreported, such as imports or specific cross-border services.

- Simplifying Taxation in Certain Sectors: In cases where it is difficult to monitor or collect tax from suppliers, especially if they are small-scale or unregistered, the mechanism simplifies tax administration by making recipients responsible for compliance.

- Reducing Evasion: By making the recipient liable, reverse charge minimizes the risk of tax evasion, particularly in cases involving imports or cross-border transactions.

Applications of Reverse Charge Mechanism

The RCM applies in the following cases:

- Import of Services: When a business imports a service from a foreign entity, GST with GST registration in Chennai is payable under RCM by the Indian recipient, as the Foreign Service provider is outside the jurisdiction of Indian GST laws.

- Specified Goods and Services: Certain goods and services are notified by the government as liable to reverse charge. For example, legal services provided by an advocate or services by a Goods Transport Agency (GTA) are taxed under RCM.

- Transactions with Unregistered Dealers: In specified cases, purchases made by a registered taxpayer from an unregistered supplier may attract GST under RCM. However, this application has been significantly narrowed down to avoid undue burden on small businesses.

Process of GST Payment under Reverse Charge

When a transaction falls under the reverse charge mechanism, the recipient must undertake the following steps:

- Self-Invoicing: Since the supplier does not charge GST, the recipient is required to generate a self-invoice for the transaction.

- Tax Payment: The recipient calculates GST at the applicable rate and pays it directly to the government through the GST portal.

- Input Tax Credit (ITC): After paying the tax, the recipient can claim ITC, provided the goods or services are used for business purposes and all conditions for availing ITC are met.

Impact of Reverse Charge on Businesses

Reverse charge has both advantages and challenges for businesses. Let’s look at both sides:

Advantages:

- Compliance Improvement: RCM ensures that taxes are paid on transactions that might otherwise escape taxation.

- Broadening Tax Base: By covering unregistered suppliers and imports, RCM increases the scope of taxable transactions.

- Transparency: It provides clarity in cases where the supplier cannot be held accountable for GST compliance.

Challenges:

- Additional Compliance Burden: Businesses must track transactions subject to RCM, generate self-invoices, and maintain accurate records.

- Cash Flow Impact: Since businesses must pay tax upfront, they may encounter cash flow issues if they cannot utilize ITC immediately.

- Complexities in Implementation: Determining which transactions fall under RCM and calculating the correct tax amount can be challenging, particularly for small businesses.

Supply: The Core Concept in GST

Supply refers to the provision of goods or services for consideration in the course of business. It is the taxable event under GST, replacing the earlier system where tax was levied on the manufacture of goods, sale, or provision of services separately.

Understanding Supply in GST

Supply under GST with GST registration in Bangalore encompasses a wide range of activities, including sales, transfers, exchanges, barters, leases, or even the provision of services without consideration under specific circumstances (deemed supplies). The key conditions for a transaction to qualify as a supply include:

- Presence of Consideration: In most cases, there must be consideration, i.e., payment, in money or kind.

- Business Connection: The parties must conduct the transaction in the course of or in furtherance of business.

- Taxable Supply: The goods or services involved must be taxable under GST laws.

Taxability of Supply

Understanding whether a supply is taxable requires careful analysis of the following factors:

- Place of Supply: Identifies the state or country where taxpayers must pay tax.

- Time of Supply: Establishes when the tax liability arises, ensuring proper reporting and payment.

- Valuation: The concept of supply is fundamental to GST, as it determines the taxability of all transactions.

Importance of Supply in GST

The concept of supply is fundamental to GST, as it determines the taxability of all transactions. Businesses must thoroughly understand what constitutes a supply and the circumstances in which it becomes taxable to ensure compliance and optimize their tax liability.

Compliance and Optimization

- Proper Classification: Misclassifying transactions can lead to penalties and interest. Businesses must ensure proper classification of goods and services.

- Efficient ITC Utilization: By understanding supply conditions, businesses can better manage their input tax credit claims, reducing tax outflows.

- Risk Mitigation: Awareness of supply rules helps businesses avoid disputes and audits by ensuring accurate tax reporting.

Conclusion

The reverse charge mechanism and the concept of supply are vital components of the GST framework, ensuring efficient tax collection and compliance. While RCM shifts the tax liability to the recipient, supply defines the taxable transactions. Together, these concepts enable the government to capture a wide range of economic activities within the tax net, promoting transparency and reducing evasion. For businesses, understanding these principles is crucial for maintaining compliance, managing tax liabilities effectively, and optimizing financial operations in the GST regime.

Recent Posts

Businesses with AATO of ₹10 Cr and above Must Report e-Invoices Within 30 Days

Starting from 1st April 2025, taxpayers with an AATO of 10 crores and above cannot…

Key Income Tax Deadlines to Meet Before March 31, 2025: Avoid Penalties and Maximize Tax Savings

As the financial year 2024-25 comes to an end, taxpayers must complete several critical income…

Key GST Deadlines before March 31, 2025

As the financial year comes to an end, businesses and taxpayers must fulfill essential GST-related…

Firms with Rs 250 crore turnover rush to register on TReDS as March 31 deadline nears

Companies with an annual turnover of ₹250 crore are actively registering on the Trade Receivables…

Accounting services in Coimbatore

In today’s fast-paced business environment, accurate and timely accounting is essential for any company’s success.…

GSTR 9 annual return

The GSTR-9 annual return is a crucial compliance requirement under the Goods and Services Tax…